To Link to a PDF version of this White Paper, please click here https://additivemanufacturingresearch.com/wp-content/uploads/2017/11/aerospacewp.pdf/images/uploads/general/AerospaceWP.pdf

Additive Manufacturing in Aerospace: Strategic Implications

SmarTech has identified four ways that the aerospace industry expects to derive value from additive manufacturing (AM) in the aerospace field at the strategic level. In this White Paper, we examine four supposedly critical aspects of AM in the aerospace industry, which are (1) reduction of lead times, (2) reduction of component weight, (3) reduction of both production and operational costs, and (4) reduction of the negative environmental impacts of production. Our research has revealed that some of these factors will be a source of great value for aerospace manufacturers over the next ten years, while others contain more fluff than substance.

The analysis in this report comes from SmarTech’s recent report “Additive Manufacturing Opportunities in the Aerospace Industry: A Ten-Year Forecast.” More details of this report can be found at https://additivemanufacturingresearch.com/reports/additive-manufacturing-opportunities-in-the-aerospace-industry-a-ten-year-forecast/ , or by contacting Rob Nolan at (804)-938-0030.

Prolog to Additive Aerospace

Aerospace manufacturers have used additive manufacturing systems since AM’s beginnings in the ’80s. But in the past few years, rapid advancements in AM technology have led applications of the technology in the aerospace industry to proliferate. AM formerly occupied a niche role in aerospace manufacturing as a technology for prototyping. As recent developments suggest, however, AM is rapidly becoming a strategic technology that will generate revenues throughout the aerospace supply chain.

Firms that are already committed to shifting the strategic dynamics of AM in the aerospace industry include: Boeing, Airbus, Lockheed Martin, Honeywell, and Pratt & Whitney. Some of the most important recent examples include:

- Airbus is exploring 90 separate cases where AM might be applied on its next generation commercial aircraft.

- GE is set to manufacture up to 100k parts with AM by 2020.

- EOS envisions a future where ten to twenty metal laser-sintering systems whir away in a production center creating large runs of end-use parts. This is a vision that GE has already started down, when it announced a $50-million investment to outfit its facility in Auburn, Alabama to manufacture its AM fuel nozzle. This announcement it seems is the first of many to come.

- Boeing already uses this technology to build everything from ducts to turbine blades to UAV parts.

As these companies continue to yield impressive results from their AM endeavors, SmarTech expects the pressure to mount for companies not currently investing in the technology to jump in so as not to be left behind. As we see it, AM will become part of the regular lexicon of aerospace engineers over the next ten years. For some projects, it will even become the go-to manufacturing technology.

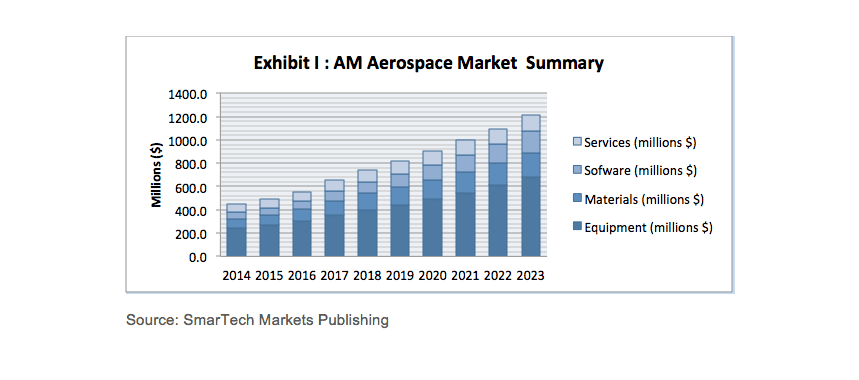

Still, there are many question marks that stand in between now and when AM will become a serious manufacturing technology in the aerospace industry. Many potential operational hurdles, such as high metal powdered material costs and a lack of in-situ monitoring systems, threaten to deflate AM’s ascendency. Such issues create confusion around the ultimate value of AM in aerospace. However after in-depth research of aerospace applications, end-users, and AM equipment manufacturers, SmarTech believes that the market for AM will indeed be substantial. The summary forecasts of our research are presented in Exhibit I below

Reducing Lead Times for Components: Greatest Source of Value

SmarTech’s analysis suggests that AM has considerable potential in aerospace. We also believe that reduced lead times for both new and replacement parts are perhaps the greatest source of value for AM in aerospace over the next ten years.

As a rule of thumb, aerospace experts now believe that AM can reduce the lead-time for a part by 80%, compared with conventional manufacturing methods. This may allow aerospace manufacturers to redesign a part up to five times more during a standard component development cycle, leading to significant performance improvements of the components.

Manufacturers are already realizing dramatic cuts in lead-time for AM produced parts. For example, Kelly Manufacturing Company was able to reduce the production time for 500 housing components from three-to-four weeks to just three days using plastic laser sintering technology. Applications like these will, we believe, create significant value for producers and customer alike over the next decade.

Meanwhile, reduced lead-time for older replacement parts can be quite valuable in commercial airliners:

- In the future, lean manufacturing with AM equipment could shift the entire inventory for aerospace parts. The ability to quickly feed a CAD/CAM design into a 3D printer and produce a part can lower the number of minimum inventory aerospace manufacturers need to keep of a part

- For commercial planes whose average life expectancy is now 30+ years, circumventing the need to maintain and replace old tooling is a notable inventory cost advantage for manufacturers. According to Airbus the turnaround for test or replacement parts can now be as low as two weeks. These parts can be rapidly shipped to and installed in a broken down plane to help get the plane back into the air and making money for the airline.

- Furthermore, the ability to incrementally scale capacity of 3DP parts by adding individual machines means that one no longer has to produce numerous extra components to recognize economies of scale in manufacturing. However, it is still very difficult to covert old part plans to digital files.

Design Improvements: The Future of Aerospace Components is Optimized

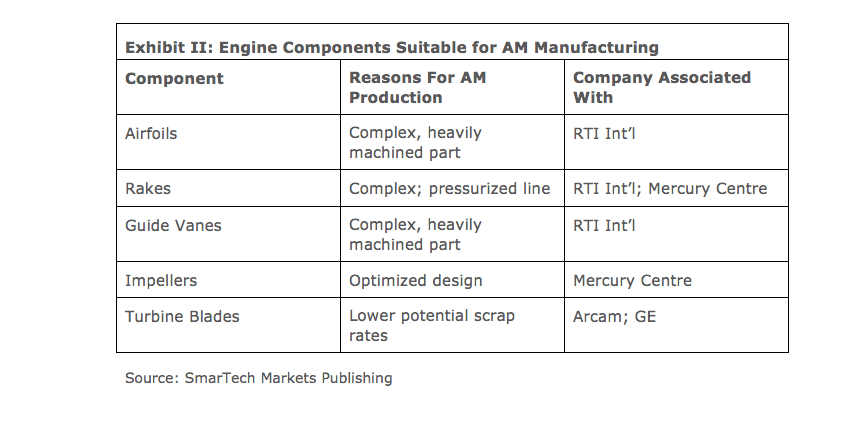

Another potential source of value in AM is through optimized design of components. AM production enables new geometries or parts that can only be build one layer at a time. These features include organic contours, lattices, internal cooling channels, and even integrated electronics. Exhibit II presents a number of high-value components whose design AM has been used to optimize in the last two years.

Many designs are improved by through radical simplification. Sub-assemblies that once had to be melded to together in many separate processes can now be printed in either a single or a few parts:

- Perhaps the most publicized example of this is the GE fuel nozzles, whose organic internal cavities reduce “coking”, or carbon build-up within the nozzle. This enhances the performance and fuel efficiency of the nozzle over time. GE engineers state that these geometries could only be realized through the AM process.

- In the F/A-18 E/F forward fuselage, Boeing was able to consolidate its design into 41% fewer parts than what they required previously. Component simplification trickles down through operational processes, further reducing costs. Fewer parts means fewer component checks and less documentation for an aircraft operator, further saving on costs.

These are dramatic developments and SmarTech expects to see more of this kind of this redesign process occurring in aerospace development over the next few years.

Reduced Component Weight: An Advantage Overstated?

Weight reduction of aerospace components carries a huge premium because airline operators can recognize the value of these reductions over the average plane’s 30+ years of operation:

- AM can undoubtedly help reduce the weight of aerospace components by printing more efficient geometries and lattice structures that carve out large amounts of unnecessary material.

- Early tests have shown that component reduction is commonly around 30% of the component weight. Thus, a study published by equipment manufacturer EOS and Airbus Group Innovation Team in February of 2014 showed that the weight of a Nacell Hinge could be reduced by 35-55% and shave 10 kgs off the entire aircraft weight.

- Nonetheless, SmarTech finds the overall opportunities to reduce aircraft weight as wholly overstated:

- Some studies have cited weight reduction of parts that are not actually airworthy. By the time such components are bulked up sufficiently to be used in an airplane, weight reduction is less impressive; on the scale of 10-20%.

- AM is limited to titanium applications. AM is not currently able to supply Aluminum 4043 parts that meet air regulation requirements

- AM can only currently address planes’ secondary structural components. This precludes the substitution of AM components for heavy primary structural components, such as wing spars.

These limitations on applications in an aircraft lower the overall weight savings attainable through AM applications. As SmarTech sees it, this is not enough to make a strong case for rapid implementation of AM parts across an airplane. This is especially true, given the fact that total weight reductions will most likely be measured against the last major weight saving initiative, which substituted advanced polymers for aluminum hulls. This initiative is posited with a 20% weight reduction over the entire plane, not just over individual components. When compared to previous weight reduction initiatives, it’s clear that AM will not easily match previous levels.

Reduce Environmental Impact: Reputation vs. Actualities

AM has often been pitched as a “green” technology. But much of the environmental benefits are realized through reducing the weight of components which, as we have already discussed, has its limitations.

Another “green” impact can also be realized through lower material consumption during the print process because only the material being formed into the object is used:

- Excess powder can be sifted and re-used, increasingly with automatic powder recovery systems attached to the 3D printers. However, the 3D print process itself is an energy intensive process.

- AM can improve buy-to-fly ratios well past an industry standard 30%. The buy-to-fly ratio is the weight ratio between the raw material used for a component and the weight of the component itself.

SmarTech believes that as many companies in the aerospace industry continue to shift strategies to become more environmentally responsible, AM’s reputation as a green technology may be more valuable than actual energy savings. The facts are that energy consumption for AM processes are quite high and don’t lead to recognizable carbon reduction in the actual manufacturing process. Furthermore, while the process may result in better material consumption rates, the high price of suitable metal powder material limits these rates from translating into cost reductions for manufacturers.

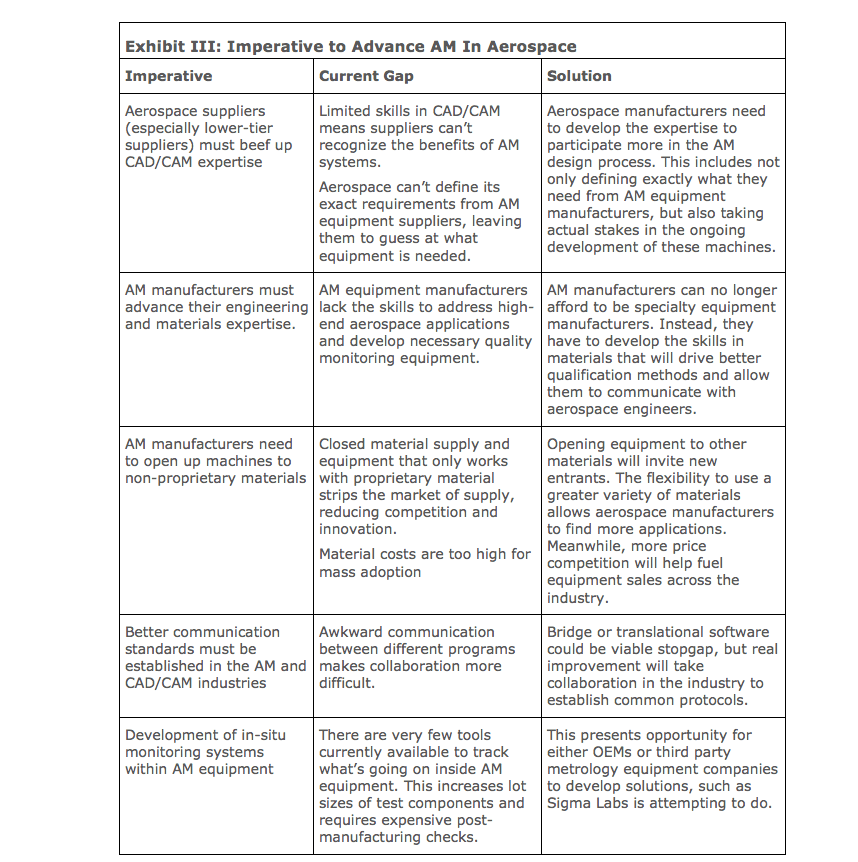

Imperatives and Challenges for AM in Aerospace Over the Next Ten Years

As shown in Exhibit III, there are many things that need to occur for AM to become a mainstream manufacturing technology in the aerospace industry. These bottlenecks hold the key to gauging future opportunities in this sector.

Then again, AM applications in aerospace face some serious challenges that may prove more resistant to solutions than those listed above. Three of the biggest challenges are:

- Extended product development cycles threaten to protract AM adoption patterns. In commercial aviation, new generation planes are designed every seven-nine years. If large enough benefits cannot be realized with AM in a given generation of planes, either because (1) the technology is not advanced enough or (2) engineers are not familiar enough with the technology, then AM might have to wait for the next plane generation to find substantial applications in the aerospace industry.

- Even more daunting is the fact that aerospace is an industry where products—that is, the planes themselves—are pre-sold up to eight years in advance. So the question is: where is the real impetus to radically change production methods at all? As the examples that are provided in this White Paper show, this factor has not proved daunting for some major aerospace companies, but might for some.

- Aerospace manufacturers may have to endure a painfully slow period where regulatory authorities get familiar with this new manufacturing process.

SmarTech expects that innovators will find unique solutions to the imperatives and challenges discussed above. This will all be accomplished with the intent of deriving value from the benefits discussed that are the focus of this White Paper. As we have indicated, we think that not all of these benefits were created equal, but they all matter. In fact, SmarTech believes that the best AM strategies that aerospace firms can deploy will be those that take advantage of several of the factors we discuss.

An obvious example of this can be found in the GE nozzle, which has become such a poster child for AM aerospace manufacturing. Here, GE was able to reduce the number of parts in the fuel nozzle, reduce weight, and improve the performance of the nozzle over time.

Final Conclusions

As we see it, all the fuss and excitement over AM in aerospace is justified. At the same time, like any business strategy implementation, an AM-centric strategy takes careful forethought that includes leveraging AM to augment aerospace manufacturing processes.

AM in aerospace therefore still has some way to go before it finds a mature strategic role as a technology for rapid manufacturing. Given the time frame at which the aerospace manufacturing business operates, it could be a decade before that maturity sets in. However, this process will be important not just to the aerospace industry, but to the AM sector as a whole. This is because the aerospace sector is, for now, the largest single source of demand for production-grade AM equipment.

In SmarTech’s report “Additive Manufacturing Opportunities in the Aerospace Industry: A Ten-Year Forecast” we break down the AM in aerospace into its most basic elements. Available equipment, industry make-up, component supply chain, key players, benefits, applications, and processes are all explored to arm our clients with the information needed to drive meaningful business decisions.